The Global Leader of Intelligent Customer Experiences

Bypass the clutter of Google. With one zip code, we instantly connect the best offers to customers who need any service anywhere in the world.

Trusted by the World’s Leading Brands

Thousands of Options. One Perfect Solution.

With the power of machine learning and human ingenuity, we connect you to the right company for any service or product you need. You can view all the best offers in one place, dramatically simplifying your search for excellent, affordable service.

TV Internet Services

Find the best TV internet plans, TV internet offers and broadband services for your zip code.

Security System

All home security systems work on the same basic principle, but not all are equal.

Moving

Leave the packing and unpacking to professional, reliable movers with established reputations.

Insurance

Secure your future with the assistance of a trusted life insurance company.

Flight and Booking

Wherever your destination is, we’re the one-stop shop for affordable flights and hotels.

Solar

Go solar with confidence. Start with a quick, free quote.

Financing

Compare rates, review the facts and get professional advice for your financial decisions.

Home Improvement

Get matched with the best home improvement professionals in your area.

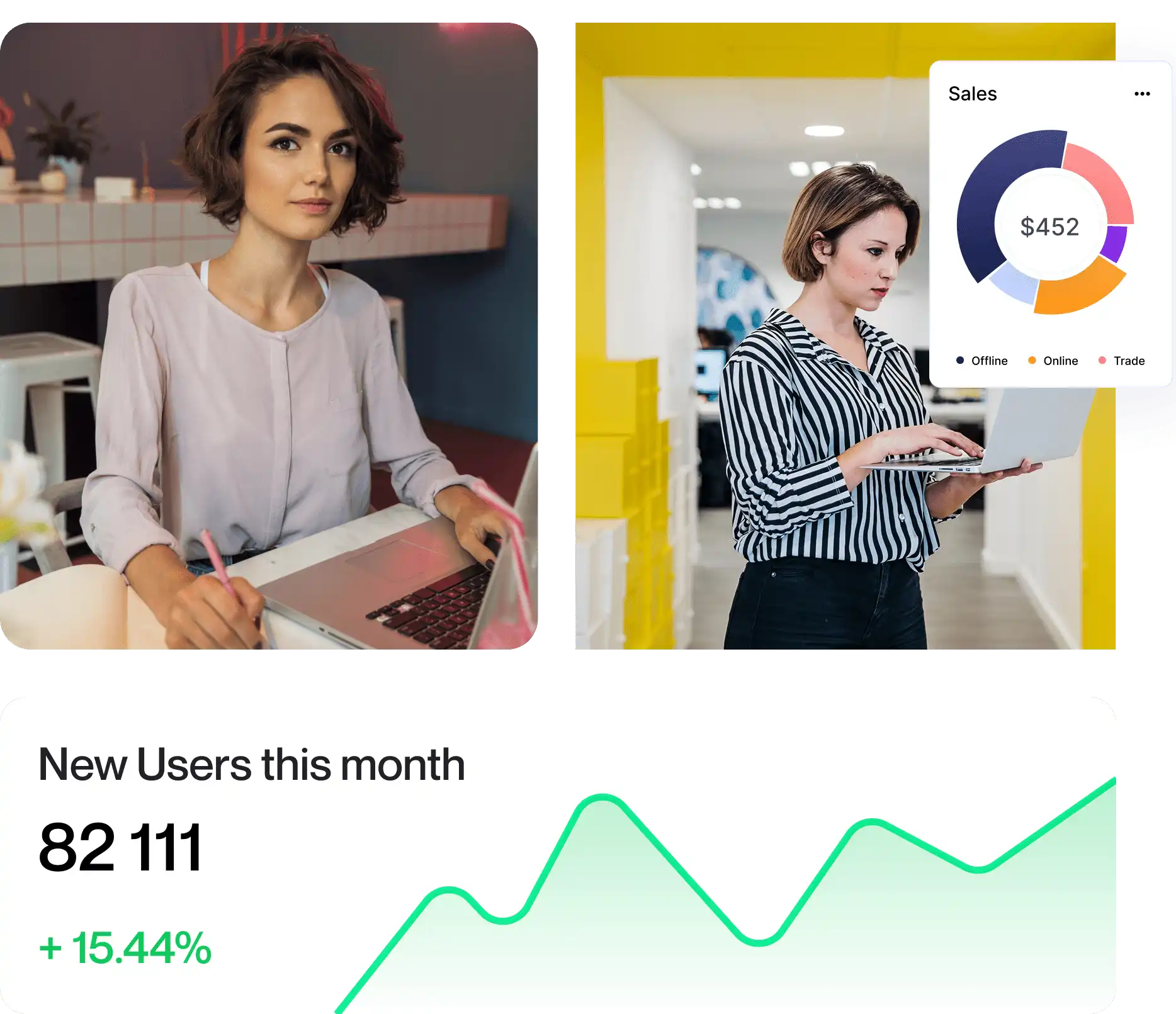

Intelligent Customer Portal

Our powerful infrastructure connects billions of data points to bring you the best solutions. We’re constantly improving our framework to keep your search results relevant, accurate, and easy to navigate.

Pointing You the Right Way

Our unique ability to bring together information from service providers around the world is what keeps our customers coming back. Whether you’re moving to a new home in another state, going on vacation, or switching internet providers, our platform gives you a wide variety of options and pricing offers all in one place.

With JNA.org, you have the power to make an informed decision based on all providers, not just those who appear first in your Google search

Case Studies From Our Marketing Experts

Best Moving Experience.

“Their estimate was one of the lower ones we came across and the final price was right in the range they gave us, which was a relief after some of the stories we’d heard about working with moving companies. With both starting new jobs and the kids starting out at a new school, it ultimately made sense to hire International Van Lines”

Our Recent Blog

July 9, 2026

Cost to Hire a Mobile App Development Agency in 2026

Discover the cost to hire a mobile app development agency, pricing factors, hidden expenses, budgeting...

Read more ↗

Learn how to build a topical authority content cluster strategy that improves SEO, strengthens internal...

Read more ↗

Discover the best time for businesses to invest in commercial solar, reduce energy costs, maximize...

Read more ↗

Discover whether solar batteries are worth the investment. Learn how battery storage saves money, provides...

Read more ↗

Learn what 100/300/100 means in auto insurance, how liability limits work, and how to compare...

Read more ↗

July 9, 2026

How to Compare Solar Energy Quotes with Confidence

Learn how to compare solar energy quotes by understanding pricing, system size, warranties, production estimates,...

Read more ↗

Compare React Native vs Flutter performance, speed, scalability, UI, and development costs to choose the...

Read more ↗

Learn the difference between manufacturer and performance warranties for solar panels, what each covers, and...

Read more ↗

Learn the difference between SEO and SEM, how each works, their benefits, costs, and when...

Read more ↗Global research.

Our research experts have rigorously compiled the best deals and data on hundreds of companies in every category. We obsess over the details so you don't have to.